The Difference between APY & APR: A Guide to Earning and Owing Infographic

We hear the terms Annual Percentage Yield and Annual Percentage Rate often in advertising, banking, and shopping. But do you know what they mean? Simply put, we’re talking interest. If you’re a little clueless about financial terms, you’re not alone. According to a 2018 survey, 48% of U.S. Americans had a hard time understanding the concept of interest.1

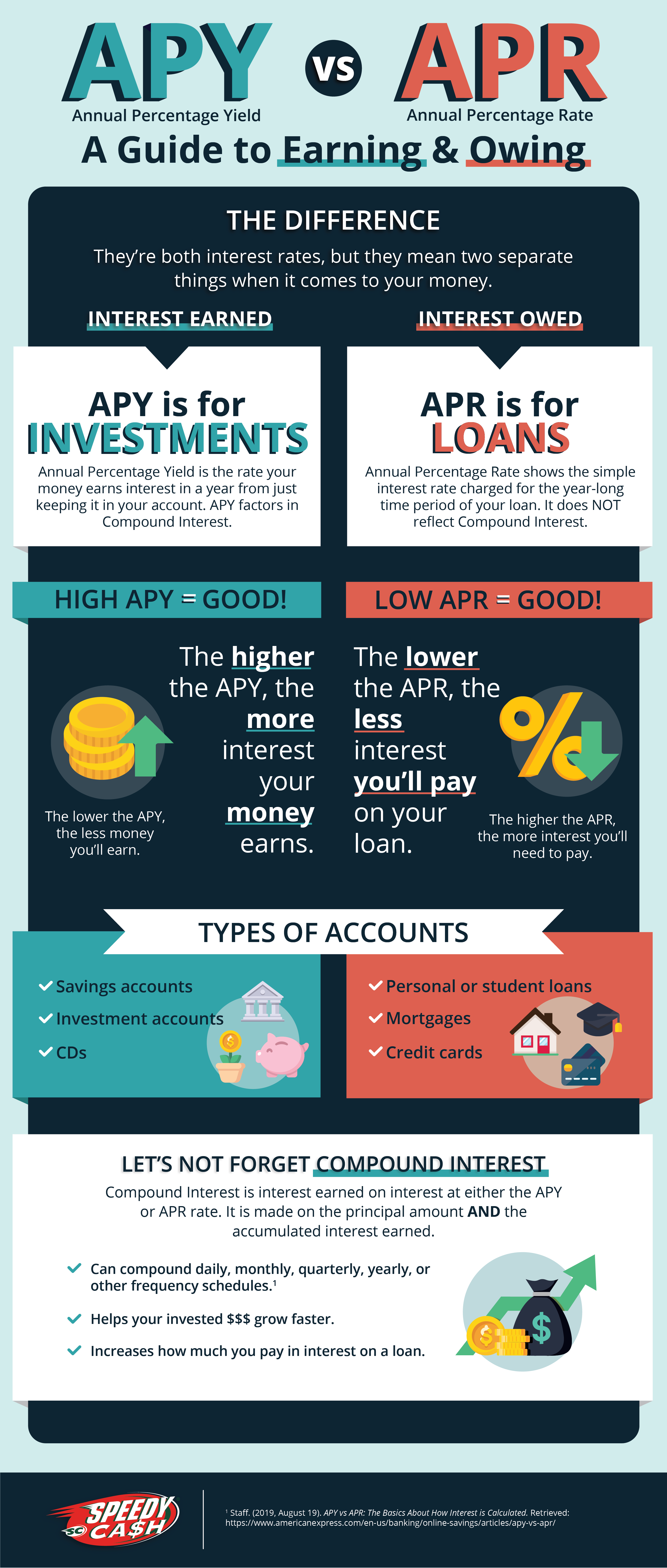

APY is interest paid. APR is interest owed. They’re both interest rates, but they mean two separate things when it comes to your money. APY is for investments and APR is for loans.

What is APY?

Annual Percentage Yield is the rate your money earns interest in a year from just keeping it in your account. This is the annual rate of return on your investment. High APY = good. The higher the APY, the more interest your money yields. This means more money for you. YAY!

As of 2021, a high APY for savings account is 0.50%. In general, savings accounts compound monthly. But this varies from bank to bank. So it’s best practice to check with your chosen financial institution.

What types of accounts have APY?

- Savings accounts

- CDs (certificate of deposit)

- Other investment accounts

The APY rate shows the total percentage amount of interest you earn from your account in a year, but also factors in frequency of compound interest. When you make deposits and leave your money in the account, the compound interest will help your money grow.

Just a sec, what’s Compound Interest?

Compound interest is made on the principal amount (your initial deposit) AND the accumulated interest you’ve made. So, it’s interest earning on interest at the APY rate. Compound interest can have varied frequencies like daily, monthly, quarterly, or yearly.2

If you’d like to personalize your numbers and dive deeper into compound interest, check out this Compound Interest Calculator, courtesy of our government.

What is APR?

Annual Percentage Rate shows the simple interest rate charged for the year-long time period of your loan. This means it only calculates interest on the principal loan amount and then could include additional costs, insurance, or fees to generate the amount of interest charges you’ll be responsible to pay. Low APR = good! The lower the APR, the less interest you’ll be paying on your loan. The higher the APR, the more interest you’ll need to pay.

What types of accounts have APR?

- Personal or student loans

- Mortgages

- Credit cards

In 2021, the average APR for personal loans is 5.95% to 30.99%. For mortgages, it’s 2.65% to 3.37%. Credit cards can have different APRs for different purchases, like travel vs. groceries. But the APR average is usually 15.56% to 22.87%. Of course, your credit score makes a difference and these rates are subject to change. But, the rate DOES NOT factor in compounding interest. So what you pay may be more (and probably will be) based on how often the compounding interest is applied. As you pay down your loan, there will be less principal and fees to compound interest on.

When talking with your bank or financial institution, read your paperwork well and ask questions. Because remember, the APR doesn’t include how often your loan interest is accruing and will be compounded. For instance, most credit cards compound interest daily. So interest charges can add up quickly!

Highlights

Here are the main points of the beasts that are APY and APR.

- The higher the APY, the more $$ you’ll earn. The lower the APY, the less $$ you’ll earn.

- The higher the APR, the more $$ you’ll owe. The lower the APR, the less $$ you’ll owe.

- APY takes into account compounding interest. APR does not.

- How often your interest is compounded (daily, monthly, quarterly, or yearly) makes a difference on how quickly your money will grow in an investment OR how much of an increase will be made on what you owe on a loan.

- When researching financial products, whether they’re investments or loans, be sure to compare APYs and APRs separately. APYs to APYs. APRs to APRs.

- As always, ask questions and read the fine print.

Getting into the thick of it

If you’re anything like me, it’s easy to get lost in the forest of financial terms and math. It’s a benefit to know how APY and APR, and don’t forget our friend Compound Interest, work. Data from an April 2020 analysis showed a large uptick in people saving due to the pandemic and acknowledging how important it is to have an emergency fund.3 So knowing the foundation of these concepts could really impact how you look at your saving accounts and loans for the better.

Sources:

- Paul, S. (2018, January 18). Americans are clueless when it comes to personal finance. Retrieved from: https://nypost.com/2018/01/18/americans-are-clueless-when-it-comes-to-personal-finance/

- Staff. (2019, August 19). APY vs APR: The Basics About How Interest is Calculated. Retrieved from: https://www.americanexpress.com/en-us/banking/online-savings/articles/apy-vs-apr/

- Bahney, A. (2020, June 4). People are saving more than ever. Here’s where to stash your cash. Retrieved from: https://www.cnn.com/2020/06/04/success/personal-savings-best-options/index.html